Read this excellent article to get a basic understanding of this whole world of selling complex instruments to municipalities:

http://seekingalpha.com/article/135193-municipalities-under-economic-stress-inside-the-muni-trading-mess?source=article_sb_picks

Home

The Macro View

Stocks & Sectors

Global Markets

ETFs

Investing Ideas

Breaking News

Transcripts

Register Login

Home » Financial Stocks » Editors' Picks, Market Outlook, Insurance, Major & Intl. Banks, Regional & Commercial Banks

Municipalities Under Economic Stress: Inside the MUNI Trading Mess 6 comments

by: Credit Trader May 05, 2009 about stocks: DB / JPM / PPM / UBS

Credit Trader

Follow

Follow.author_sidebar__follow_button_initiator('credit-trader')

25 Followers

1 Following

You are currently following Credit TraderStop Following

You are no longer following Credit TraderAbout this author:

Credit Trader's articles on Seeking Alpha

Visit: A Credit Trader Become a Contributor Submit an Article

TweetThis

Trades are going sour and the municipalities are rebelling…

Milan Police Seize UBS, JPMorgan, Deutsche Bank Funds

JPMorgan, 11 others sued over Jefferson county crisis

Derivatives Hit Austrian Railroad With Record Loss

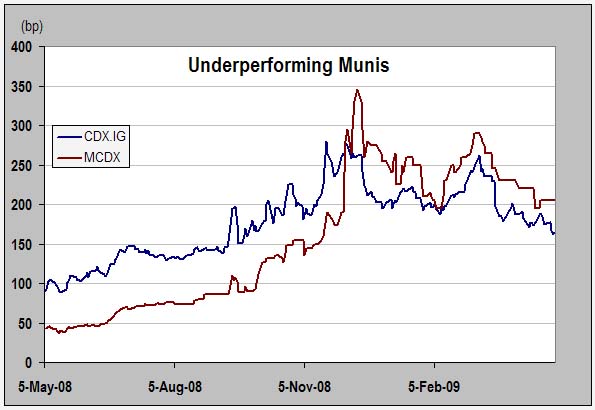

… and market spreads are responding (click to enlarge)

implying default rates that illustrate to what extent the market is dislocated.

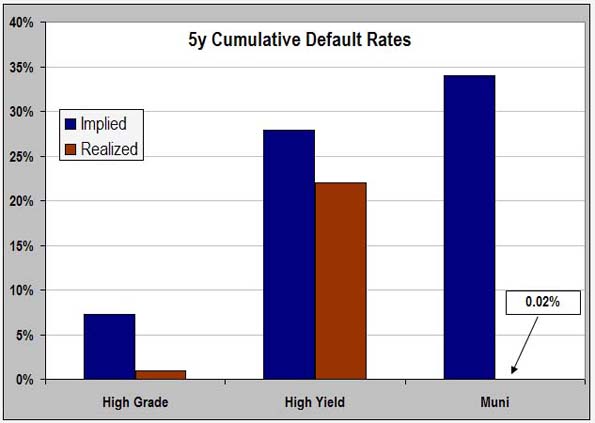

Find the one that doesn’t fitMunicipal CDS market spreads (via the MCDX index, click to enlarge) imply a 5y cumulative default probability of 34% versus a historical default rate of 0.02% (Moody’s) - a figure 1500x higher!

Purists in the room will claim that we cannot rely on a rating agency for historical default rates, as statistics come only from rated issues. Additionally, the default numbers do not take into account conduits where the default rate can run 10x higher – in fact, 2008 alone saw over $6bn of muni defaults – 19x higher than the previous year, though this has been in non-GO and unrated issues all of which recovered at 100% (anyone involved in the CDO market would laugh at a “default” that recovered at 100%, having been inured to the trusty old 0%).

The high market implied default rate is also skewed by the high expected (marked) recovery for muni bonds of 80% versus 40% in high grade (a higher recovery implies a higher default rate for a given CDS spread level) as well as potential uncertainty over deliverable obligations into muni CDS.

Each down cycle in markets exposes those unsophisticated investors who are “swimming naked”. Municipalities tend to be perfect examples as the Lack of Sophistication / Assets Under Management quotient is strikingly high. Though the current crisis is presenting muni’s with more than badly gone trades, it is these trades that offer the biggest lessons to investors.

Below I walk through what has gone wrong and what lessons have been learned (or relearned). In particular, I suggest the following guidelines to both the municipalities that have gone off the trading deep end as well as the banks that have assisted in the process.

Suggested Guidelines (fleshed out below)

Investment guidelines for municipalities:

Take no basis risk

Use no leverage

Make no punts

Risk management guidelines for banks:

Do not offer double-down trades

Pay attention to “willingness to pay”

Use credit mitigants like collateral and mark-to-market trigger agreements

Munis under stressThough Muni spreads are clearly too high, it is equally true that many municipalities are under economic stress. In April, Moody’s assigned a blanket negative outlook to the entire U.S Local Government sector, citing fiscal challenges as a result of the housing market collapse, dislocations in financial markets, and a deep recession.

Total fiscal 2009 budget deficits stood at $72bn, or 12% of general fund assets, according to the Center on Budget and Policy Priorities

Decline in state revenues is accelerating due to a decline in sales and tax receipts

Tight capital markets are constraining raising funds, though issuance has recovered since the Lehman default

States are facing challenges with their pension obligations just as falling equity and corporate bond prices have eaten into investment pools

With Jefferson county teetering on the edge of Chapter 9, Vallejo, Calif recently entered Chapter 9 protection. Other California cities, including Rio Vista and Iselton have also said that budget gaps may force them into insolvency.

Outside of the difficult economic environment, munis have also been embroiled in their own financial mess, involving VRDO’s, TOBs as well as the monoline insurance disaster all of which are putting additional pressure on finances. In fact, trading decisions made by municipalities now figure in municipal investor analysis just as strongly as fundamental indicators like unemployment, interest expense and general revenue.

The Brave New World of Muni TradingBelow I list the trades executed by municipalities that have been particularly prominent in the news.

VRDNsThe most interesting trade to come out of the muni crisis has been the debacle seen in the variable rate market. The two types of variable rate muni securities are VRDOs and ARS. They are broadly similar but vary in puttability (VRDO’s are puttable, ARS’s are not), denominations, monoline coverage, investor types etc.

The most important thing, which is common to both types of securities, is that the interest rate resets periodically according to some basic rules (auction-failure for ARS or a result of the remarketing process/changes in specified index for VRDO). The interest rate resets either to whatever rate clears the market or in the case of auction failure, steps up to a very high level so as to compensate those investors who were not able to sell their securities. These securities were very popular with muni issuers simply because, even after all the structuring fees (bank letter-of-credits and monoline insurance), the variable short-term rates paid by issuers were less than if they had issued long-term fixed rate debt.

The rates paid on the VRDO’s have tended to track the front-end cash/Libor levels. For this reason, the municipalities, bowing to the wisdom of risk management, hedged their interest rate exposure by paying fixed on interest rate swaps (or buying interest-rate caps). The floating index on the swaps was typically 67% of Libor. So, in the ideal case, the muni is paying a floating rate while receiving pretty much the same rate on its swap hedge on which it pays fixed.

When the market grew suspicious of monolines, participants rushed to put the bonds back to the market just as the bids retreated from auctions. Clearing rate levels shot up and ARS’s hit their maximum rates – most well-known is the case of Port Authority which started paying 20% vs. an earlier 4%.

So, the net result was that the floating rates the muni’s were paying on their VRDN’s shot up (owing to general illiquidity as well as the concern around monolines), while the floating rates they were receiving on the swaps collapsed (as interest rates fell) – meaning the muni’s managed to lose money both on their bonds as well as the hedges.

In retrospect, the municipalities made a number of key mistakes:

Liquidity risk – the most fundamental mistake was similar to the one that befell the Structured Investment Vehicles: the reliance on short-term debt. Once cracks appeared in the monoline wraps and investors withdrew into cash, the muni’s were not able to roll over their debt. The municipalities were effectively subsidizing the rate on their debt by writing a massive liquidity option. They compounded the problem by backstopping their own short-term debt with impossibly high rates, knowing full well that paying such rates on their debt was not sustainable. The realization by the market of lack of demand for variable-rate securities and the unsustainably high rates paid on the debt only added to the lack of confidence in muni debt

Monolines – anything having to do with monoline wraps tends to be procyclical meaning it will exaggerate the pain on the wrapped products. The basic point is that the nature of the monoline business suggested that the time when an investor will seek to benefit from the wrap, is exactly time when that wrap will be worthless. Apparently, some municipalities have also agreed to post collateral in the case of ratings downgrades, something which would tend to happen when the monolines are gone, the economy is in recession and cash is at a premium and difficult to raise and swaps are negative-MTM to the muni’s.

Rates – municipalities may be forgiven for failing to foresee the silly price action in 30y swap rates which are still trading below 30y treasury yields. This was due to hedging of structured rate notes by dealers issued mostly to individual investors. The massive rally in rates has led banks to receive fixed in size in the long end of the swap curve in a largely illiquid market. This has led to large losses to the swap hedges done by municipalities. Most of these have tended to be in the long end of the curve, just where the rally has been most brutal.

Selling swaptionsSecond on the list of poorly-thought-out trades has been the selling of interest rate swaptions. On the face of it, the motivation for selling swaptions looks quite reasonable. The muni issuer sells a payer swaption (on exercise the muni will pay the fixed strike). If the swaption is exercised, the muni pays fixed, receives floating and at the same time issues floating-rate bonds and uses the proceeds to refund the outstanding issue of bonds. Net result is a locked in synthetic rate for the issuer with some savings from the swaption premium.

This all sounds well and good except for the fact that the banks end up dictating if and when the municipalities issue debt. This decision to issue debt is not based on any fundamental funding need, but rather on the performance of a single trade done with the bank.

A cursory look through the news shows that Erie School District, Philadelphia National Airport and Alabama Schools have all sold swaptions. This suggests that if rates were to fall they, and many other counties and districts who have also sold swaptions would need to come to the market and issue debt, leading to potential supply dislocations.

Structured NotesThis round of municipal crises has been (yet?) notably clear of structured note exposure, unlike the Orange County episode. Recall that Robert Citron put a large part of the portfolio into structured notes, particularly, inverse floaters. In fact, the county bought more inverse floaters (in notional terms) than there was equity in the fund. In the end, it was the leverage (about 2.6 at the highs), financed via reverse repos, that largely led to the $2bn of losses for the fund.

The particular danger in inverse floaters has to do with their duration profile. As inverse floaters are floating-rate products (the rate is linked to the level of interest rates), one would be forgiven in thinking they have short duration. In fact, the duration is higher than for a similar-tenor fixed-rate bond and increases as the trade goes against the investor (i.e. it starts behaving more like a zero-coupon bond).

What blew up Citron was the fact that he took on two kinds of leverage (you could say, he tripled-down): 1) the particular investment that he chose to express his views – the inverse floater was already dollar-for-dollar a leveraged investment as the duration of the product increased precisely when it went against Citron and 2) Citron put more money into inverse floaters than there was equity in the fund.

In addition to leverage and unappealing duration risk, the county had credit exposure to the dealers which was less of a concern then but is clearly much more significant now. In fact, given the current experience, real money investors are much more likely to structure trades with SPV’s rather than dealers directly in the future.

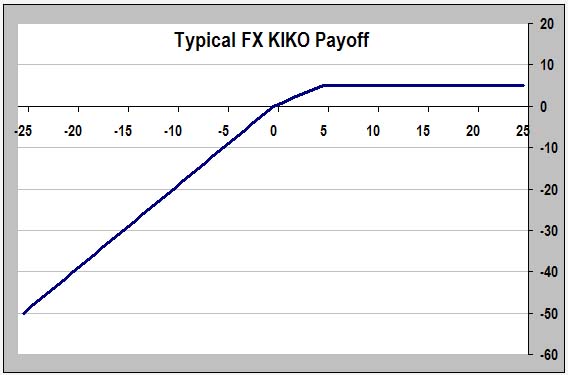

FX KIKOsFX KIKO trades are the latest in the long series of toxic trades executed by unwitting investors during the latest market cycle. In fact, they have been so popular that they’ve been described in Bloomberg magazine, where they were called “I-kill-you-laters”, rather than “Accumulators” – their traditional pre-crisis name.

Though rumors of potential pain by European municipalities is only beginning, recent victims include corporates like Gruma (GMK) – the world’s leading tortilla manufacturer with $700mm losses on the Mexican peso, Citic - with losses of $2.7bn on the Aussie dollar as well as countless other companies and investment houses. Although they come in different variations, these are essentially carry trades with some additional bells and whistles (or, if you like, smoke and mirrors).

Without going into detail, the basic structure of the trade can be summarized by the following chart (click to enlarge).Salient points of this trade are the following:

If the market goes in the client’s favor, they make a little money and the trade matures in short order

If the market goes against the client, the notional amount on the trade increases and the maturity extends.

Exporters who did the trades claimed they were being done for hedging purposes. For example, a Mexican company exporting tortillas to the US market received dollars and needed a product that effectively made them short USD/MXN (ie whereby they sold dollars and bought pesos in the market). It is true that these trades positioned these companies the right way, unfortunately the trades were done in much larger size than the hedging operations required and the timing (knock-out components) plus leverage on the trades (which typically flipped from 1 to 2x the size when it went against the client) had no fundamental bearing on the actual financial flows.

It’s not clear how popular this trade was with municipalities though history of municipal involvement with FX stretches all the way back to 1995 when the State of Wisconsin Investment Board lost $95mm from MXN peso trades. Add to this the fact that municipalities pile in, along with companies and retail investors, into popular trades at the top of the market suggests that should see losses on such trades may be disclosed soon enough.

CategoriesThe classification of the trades described above can be summarized as follows:

Basis Risk – these are trades done for fundamental reasons, like obtaining cheaper funding, but go sour occasionally because they expose the investor to some tail risk. VDRN’s was one such trade that exposed muni’s to tail funding/liquidity risk as described above. The key here is to understand that the only reason muni’s were cheapening their funding was by selling a liquidity option to the market. So long that these tail options are viewed as risk free, municipalities will continue making the same mistakes. In reality, nothing is free in the market, and issuance decisions will be made on a more sound basis in the future if all risks are properly taken into account rather than swept under the rug.

Leverage – these are the typical “investment” trades based on a particular view of the market. The danger lies in the execution of the view (e.g. structured notes), as well as the leverage taken separately by the investors (via reverse repo’s).

Punts – these are trades done for apparently “investment” or “hedging” reasons. What differentiates punts from normal investment trades is the fact that the punt is done in a market where the investor can have no competitive advantage or insight relative to other players in the market. In other words, the answer to Ken Fisher’s question “What do I know that others don’t?” cannot be answered satisfactorily. These trades often figure in FX markets and often executed long after the popular press begins writing about their virtues. The FX KIKO, which is based on the carry trade, is an example of such a trade.

ConclusionIn order for the market to move beyond the news cycle of losses by municipalities and other unsophisticated real money investors, there need to be some fundamental changes. These changes have to come from both sides of the equation: municipality investment mandates and bank risk management policies.

Recent news has made it painfully clear that municipalities need to abstain from certain kinds of risks. These risks include the 3 categories mentioned above because each one has the potential to bury them, if left unchecked. In general, municipalities do not have the resources to run a full-fledged asset management organization, suggesting that their investment mandates need to shrink significantly. Although, generally speaking, the allocation of more power and decision-making ability to the local levels is not a bad thing, what we cannot have is a situation where part-time town board members without strong and dedicated risk management support staff make decisions that put at risk pensions of thousands of other people, while guided by biased investment advisors.

Investment mandates for municipalities need to be made on a state, if not the federal level and there has to exist a framework for escalating problems higher up before they explode. For example, a county finding itself in financial difficulties should not think that the only way out of trouble is to finance its budget by selling a ton of swaptions to the next friendly dealer that comes along.

On the bank side, dealers need to adapt consistent trading and “know-your-client” standards with municipal counterparties. These should not only include a relatively conservative set of products, but also collateral calls so that “punts” and leveraged trades, to the extent they are allowed to happen at all, are unwound/collateralized early and are treated with more care and tracked closely.

The traditional treatment of counterparty risk does not hold for unsophisticated investors like municipalities who can easily claim in court (often with good reason) that they did not understand the risks in the trades they were doing. Clearly, this will happen only when trades go bad adding its own particular wrong-way risk to these trades for banks.

There needs to be greater emphasis placed on the motivation behind client decisions to do certain trades. For example, an interest rate position done for genuine hedging of risk (preferrably without any basis risk) is very different from a short swaption position done to raise cash. The latter is a clear red flag and suggests that the client is essentially doubling down to get out of a financial jam. The risk management function of the banks should ensure that such trades are not done.

SeekingAlpha.Initializer.LogAndRun(load_article_toolbar);

Related Articles

Independent Analyst Numbers Far Uglier Than Official Stress Test Rumors Quick Read May 06, 2009

Private Equity to Rev Up With Chrysler's Bankruptcy? Quick Read May 06, 2009

IntercontinentalExchange Sharply Higher on Earnings Quick Read May 06, 2009

Ken Lewis: Whistleblower? Quick Read May 06, 2009

Stress Test Results Seem to Be Changing Daily Quick Read May 06, 2009

remove_unneeded_article_from_article_more_box(135629);

Related Stocks:

DB, JPM, PPM, UBS

Stock Alerts

Get free stock alerts by email:

DB

JPM

PPM

UBS

We don't spam

SeekingAlpha.Initializer.LogAndRun(create_new_advert_box);

Print this article with comments

var ratings_hash={}, top_commenters_array = [];

ratings_hash = { 490575: [1,0], 490668: [1,0], 490887: [2,0] };

top_commenters_array = [98115,274708,265539,226469,317799,199165,227454,242427,224836,338690,142670,343824,206839,104402,182679,117436,287539,336913,223450,236295,283977,86092,349306,329934,353732,297968,173953,194962,393700,262977,333610,84036,259051,135117,365912,214245,199626,337397,240305,317592,204402,372226,294123,239719,366570,275579,269895,317013,175609,356415,353239,56572,315437,329631,289443,282191,85985,159453,225115,302824,265323,368181,350335,175946,351063,117414,192595,338683,249534,342265,327853,223675,198185,305657,161568,22392,204260,111272,135017,169560,162115,305589,336628,186512,308029,135406,134986,358942,177447,341510,298836,375853,185815,192912,358080,250659,201406,248498,364357,223943];

This article has 6 comments:

SeekingAlpha.Initializer.LogAndRun(function () { notice_to_element("comments_list","update"); })

Register or Login to rate comments »

masf

4 Comments

Follow.comment__follow_button_initiator('400169', 'comment_490575')

Follow

Questions: Are you saying the municipalities themselves didn't understand what they were getting into? Also, are you talking about the kinds of bond issues people vote for in special elections? Thank you.

May 05 01:33 PM Link

nobby73

62 Comments

Follow.comment__follow_button_initiator('380678', 'comment_490643')

Follow

Very good analysis, especially the description of the products. Some of the transactions executed by munis are hair-raising to say the least. The VRDN structure is toxic. You describe it as liquidity risk, but you could say it is credit risk - as the market conditions worsen, the coupon steps up, thereby increasing costs and accelerating default. When you discuss the "know your client" analysis of the banks, I think you are being kind. You seem to suggest the banks should have done their homework and realized the munis are not sophisticated. I would love to see the presentations the banks showed. I very much doubt they had a section saying, this is a floating bond and this is a swap to put the rate back to fixed. I would imagine the products shown to munis were only highly complex but presented in a way to suggest that this was what everyone was doing.Anyway, I digress, the solution is very simply. No embedded optionality of any sort, in bonds or swaps. No collateral agreements (therefore the banks have to be prepared to take the full risk).The purpose of derivatives are for liability management and they must be risk reducing - it does not take a genius to work out what is risk reducing, you simply compare revenue streams to interest costs. The swaps may give the banks a credit exposure but if it reduces the overall risk to the issuer, then this is ok, but forget about monoliners, this simply creates the illusion of protection. What is clear is banks pushed the riskiest of products, but I don't understand the motive of the financial teams at the munis who thought it was a good idea, but they should ask themselves if they think they are so smart, why aren't they working on Wall Street - or maybe they thought doing something funky might help them get a job on Wall Street?Seems to me that banks need to be taught a lesson and if they are not prepared to actually help the munis they need to be legally prevented from doing business with them.It needs to be stated very clearly, between the banks and the munis, they are gambling with the tax payers money.

May 05 02:13 PM Link

everyothercatstaken

20 Comments

Follow.comment__follow_button_initiator('359016', 'comment_490668')

Follow

It seems to me increasing muni(as well as state and county) credit risk will become more apparent soon. Anyone ask a public sector employee or retiree lately about the adequacy of their pension fund assets?I have. No one has yet to have seen a report, though quite a few have asked and not been satisfied.And yet public sector budget goals have not been met, the equity and real estate markets which embrace their pension fund investments are down sharply, and costs(mostly salaries and pension obligations) are escalating. One of our next shoes to drop?

May 05 02:28 PM Link

Socialism cannot compete!

800 Comments

Follow.comment__follow_button_initiator('135812', 'comment_490887')

Follow

My town in the last 18 months passed a referendum to build a new high school -- for $96 million!!! The dumb-wads in town hall continued to press forward even after this financial collapse began. Construction is now underway. Muni bonds will have been issued, of course, to pay for the deal. It is truly a monstrous, theme park of a school -- there is NO WAY what they are building is necessary!! Delusions of grandeur prevail in this town. And I have a feeling it will come home to roost SOON, as they may not be able to pay back their debt. Who will move into a town with the mill rate they are going to impose? 'Cuz let's not kid ourselves -- given home value reassessments, there are two ways to make up the difference: get more people and businesses to move here, or jack up the mill rate to make up for lower valuations. It will be the latter.And so, I believe, the story will unfold all across this land: the next BIG SHOE TO DROP will be at the local level, with people refusing or unable to pay the huge tax bills that are going to be foisted upon them. And cities will default on their munis.

May 05 04:24 PM Link

dybydx

88 Comments

Follow.comment__follow_button_initiator('383421', 'comment_491275')

Follow

is it really possible for munis to default? i mean... it would be odd to see Sacremento files for chapter 11 or god forbid.... chapter 7?i personally would not mind to buy munis, watch them default and demand the golden gate bridge as in kind payment. i'd be rich from the toll collection.

May 05 10:35 PM Link Reply

willydo

10 Comments

Website

Follow.comment__follow_button_initiator('223006', 'comment_491291')

Follow

I think what the article says is basically all good information. However, when I have done recent scans of funds and etf's crossing their 200 day MA, they are DOMINATED by muni bond funds. In fact, I have never seen such a concentrated move in a single sector. Apparently a lot of investors don't think the muni's will default. I'm not saying they know what is true but wow, the money going into them now is amazing. I think a lot of people are looking to lock in the 6-7% tax free yield (most think taxes will be going up..uh..uh) and that is for the Insured Funds. (I know some people think the insurance co's can't actually pay....but that's another issue). I currently have IMT, NZF, and FHIGX but I guess I can sell if things get too bad. On the other hand, if the gov'ts efforts at reviving our economy work, we'll have these yields locked in (imho).Thanks, Willydo (by the way, how do I trigger notification to read other responses to this article or do I just have to keep "chekin' back"??

May 05 11:02 PM Link Reply

Most Popular

The Worst Case Scenario (Someone Has to Say It) Quick Read

Wall Street Breakfast: Must-Know News Quick Read

Why This Rally Is Unsustainable Quick Read

DirecTV / Liberty Entertainment Merging: Why This Affects Sirius XM Quick Read

22 Dividend Stocks with Good Fundamentals Quick Read

Tuesday Outlook: Where's the Volume? Quick Read

Why Did Dendreon Execs Cash Out on Friday? Quick Read

Sirius on the Move: Purely Technical? Quick Read

Stress Test Leaks: Endgame Emerging Quick Read

10 Highest Paid CEOs for 2008: Unbelievable Quick Read

Editors' Picks

Debt, Doubt, and Disease in the Markets Quick Read

Independent Analyst Numbers Far Uglier Than Official Stress Test Rumors Quick Read

Predicting Stress Test Outcomes Quick Read

We Need to Make Banking Boring Again Quick Read

California: More than Just Economic Problems (Plus Some Potential Solutions) Quick Read

Sign up for Seeking Alpha RSS Feeds

Related Themes:

Market Outlook (138 in last week)

Insurance (9 in last week)

Major & Intl. Banks (103 in last week)

Regional & Commercial Banks (37 in last week)

Bonds (37 in last week)

More by Credit Trader

Risk Management Watch: The Monoline Insurance Delusion

on Apr 06, 2009 Quick Read

Big Bang Theory: Fixing Annuity Risk by Recouponing CDS

on Mar 31, 2009 Quick Read

CDS Recoveries: Down and Out

on Mar 28, 2009 • C Quick Read

remove_current_article_more_by_author_sidebar()

The Seeking Alpha 100

The top 100 stockmarket authorsselected for publication

1

David Fry

2

Peter Schiff

3

Don Dion

4

Philip Davis

5

Bespoke Investmen... See all Seeking Alpha 100 »

Fastest Climbers

Authors with the largestincrease in followersin the last 7 days

1

Naufal Sanaullah

2

David Fry

3

Cliff Wachtel

4

Tyler Durden

5

TraderMark See all Fastest Climbers »

Top Commenters

Top commenters,as ranked by their peers

1

John Lounsbury

2

prudentinvestor

3

Moon Kil Woong

4

Steven Hansen

5

CautiousInvestor See all Top Commenters »

Top Instabloggers

The 100 most activeInstabloggers.

1

Jack Haddad

2

Mad Hedge Fund Tr...

3

dividendgrowthinv...

4

The Manual of Ideas

5

Angelo Grigoropou... See all Top Instabloggers »

Contributors

How to become a contributor

Contributor benefits

What is Seeking Alpha Certified?

Feature your company/blog/book

Interview a contributor

What's New?

What's new at Seeking Alpha?

About Seeking Alpha

About us

Wednesday, May 6, 2009

{kind=link}

{kind=link}

{kind=link}

Labels

- Civil Society (478)

- Liar's Poker by Michael Lewis (342)

- Hot Air (327)

- Heating Degree Days (160)

- Good Writing (153)

- natural gas (148)

- Deregulation of Electricity (139)

- Cramer Yesterday (134)

- Paul Krugman (128)

- Masters of the Universe (102)

- baselinescenerio.com (101)

- Countrywide (95)

- madoff (88)

- tech tips (76)

- aggregation (72)

- health care (63)

- trading again (63)

- Saakashvilli (59)

- Duke Energy (58)

- Trading Natural Gas and Other Futures and Derivatives (58)

- bailout (55)

- friedman (53)

- David Brooks (52)

- e-bills (52)

- Not Hot Air (51)

- simon johnson (50)

- Home Buyer (45)

- goldman sachs. (45)

- Leverage (43)

- Bear Stearns (39)

- Gretchen Morgenson (36)

- aig (36)

- herbert (35)

- real estate (33)

- GE (29)

- derivatives (29)

- Cramer Today (28)

- confessions of a pattern day-trader (28)

- gs (28)

- 885 Greenville (27)

- etf's (27)

- brooks (26)

- CNBC Today (25)

- Crash of 1987 (24)

- Rush Limbaugh (24)

- rich (23)

- How to Read This Blog (22)

- saackashvili (22)

- crash now (21)

- Clarence Thomas (20)

- kristoff (20)

- Nocera (19)

- William F. Buckley Jr. (18)

- cohen (17)

- credit default swaps (17)

- dowd (17)

- lehman (17)

- The Big Short by Michael Lewis (16)

- citicorp (16)

- hedge funds (16)

- obama (16)

- Charlie Rose (15)

- collins (15)

- cramer last night (15)

- globe_mail (15)

- banks (14)

- dreier (14)

- flynn's oil (14)

- georgia (14)

- kristol (14)

- Banc of America (13)

- Cramer and October 8 (13)

- Gold (13)

- Jimmy Rogers (13)

- The Current Stock Market and Reporting Therein (13)

- Warren Buffett (13)

- geithner (13)

- Bill Gross (12)

- Norris (12)

- Value of Diversification (12)

- c (12)

- fifth third (12)

- stimulus plan (12)

- American Energy (11)

- Auchincloss (11)

- bill moyers (11)

- david f swensen (11)

- humor (11)

- margaret wente (11)

- nakedshorts (11)

- pattern day trader (11)

- Ah Enron (10)

- alternative investments (10)

- yale (10)

- Energy Savings for Residential Home (9)

- Paulson (9)

- aig.credit default swaps (9)

- bond funds (9)

- investment advisors (9)

- realtors(R) (9)

- toxic (9)

- Misleading CNBC Ads (8)

- Why I Was Too Busy (8)

- canada (8)

- carlos celdran (8)

- consuelo mack (8)

- dead_of_winter (8)

- fifth_third (8)

- jp morgan (8)

- larry summers (8)

- morgan stanley (8)

- rubin (8)

- wolfe (8)

- Amaranth (7)

- Barefoot Advertising (7)

- Cooling Degree Days (7)

- Glengarry (7)

- Judge Cudahy (7)

- No Hot Air smart grid (7)

- Weakening Dollar (7)

- james kwak (7)

- pogue (7)

- reflects (7)

- symmes township (7)

- what we learn when special people die (7)

- Municipality Bankruptcies (6)

- Notary Signing Agents (6)

- Private Equity (6)

- andrew ross serkin (6)

- bogle of vanguard (6)

- civil rights (6)

- fannie and freddie (6)

- gm (6)

- health (6)

- italy (6)

- keynes (6)

- mortgage brokers (6)

- stan chesley (6)

- susan boyle (6)

- volker (6)

- ; CNBC Today (5)

- Actual Laurel and Greenville (5)

- Cost Per Megawatt (5)

- Deregulation (5)

- Judith Warner (5)

- Merrill Lynch (5)

- Phil Gramm (5)

- The Dollar (5)

- auction rate securities (5)

- bonds (5)

- cramer's crash checklist 2010 (5)

- credit cards (5)

- dan gearino (5)

- dominion (5)

- dulley (5)

- high frequency trading (5)

- iou (5)

- iran (5)

- john lanchester (5)

- joseph cassano (5)

- kesselschlacht (5)

- libor (5)

- mybesttime (5)

- natural gas is not like oil (5)

- palin (5)

- philippines (5)

- sec (5)

- stanford (5)

- ted kennedy (5)

- Gail Collins (4)

- Hunter S. Thompson (4)

- Si burick (4)

- US Dollar (4)

- art cashin (4)

- blow (4)

- buffett (4)

- don marshall (4)

- dwell (4)

- economics (4)

- finances (4)

- fraud (4)

- green township (4)

- grisham (4)

- harry markopolos (4)

- heating oil (4)

- hillary (4)

- investment banks (4)

- john c bogle (4)

- pajama traders (4)

- rider fpp (4)

- soros. friedman (4)

- sotomayor (4)

- subprime meltdown (4)

- supreme court (4)

- tarp (4)

- where we live out lives (4)

- 1998 (3)

- 970 laurel (3)

- Fiscal Stimulous (3)

- Paul Newman (3)

- Reich (3)

- The Associate (3)

- Thomas Frank (3)

- What a Ride Ye Gave Thee Shareholders (3)

- ackman (3)

- bp (3)

- burry (3)

- calvin trillin (3)

- carlos slim. masters of the universe (3)

- cdo (3)

- cds's (3)

- checklist (3)

- christopher buckley (3)

- collapse (3)

- commodities (3)

- david muth (3)

- doug worple (3)

- duhigg (3)

- duke energy retail sales llc (3)

- elizabeth warren (3)

- euro (3)

- flash crash (3)

- g-20 (3)

- glendale (3)

- goolsbee (3)

- gs; Liar's Poker by Michael Lewis (3)

- gs; goldman sachs. (3)

- hank greenberg (3)

- institutional investor (3)

- insurance companies (3)

- law firms (3)

- manila (3)

- mcnees (3)

- meredith whitney (3)

- middle east (3)

- movies (3)

- new yorker (3)

- option arms (3)

- paul daugherty (3)

- procter (3)

- reagan (3)

- ritchard posner (3)

- steve martin (3)

- stimulous plan (3)

- terrorism (3)

- toqueville (3)

- trust (3)

- wendell potter (3)

- words (3)

- Bernie schaeffer (2)

- Buddy (2)

- Editor's Selection (2)

- Frank DeFord (2)

- Gasparino (2)

- George Vecsey (2)

- Geothermal (2)

- God (2)

- Greenspan (2)

- Latest Carry Trade (2)

- Railroads (2)

- Remnick (2)

- Rich.reflects (2)

- Spitzer (2)

- The Very Crux (2)

- Wachovia (2)

- Weather Futures (2)

- a heddgie (2)

- abacus (2)

- aep (2)

- andreww ross serkin (2)

- arthur nadel (2)

- auto task force (2)

- barcelona (2)

- barrons (2)

- barton (2)

- bernanke (2)

- beth smith (2)

- biden (2)

- bill black (2)

- black swan (2)

- blood pressure (2)

- bridge (2)

- brooks-Simon (2)

- bruce abel (2)

- bubbles (2)

- cheever (2)

- chris dodd (2)

- christopher walken (2)

- community reinvestment act (2)

- corporate bonds (2)

- cramer's list (2)

- crash of 1929 (2)

- crash of 2:45 p.m. (2)

- cursing mommy (2)

- daugherty (2)

- donttrythisonyourhome.blogspot.com (2)

- duk (2)

- economix (2)

- entrepreneur (2)

- eu (2)

- fasb (2)

- fast money last night (2)

- financial advisors (2)

- financial crisis inquiry commission (2)

- fool's gold (2)

- glanville (2)

- glass-steagall (2)

- guessing cramer (2)

- hal mcCoy (2)

- house of cards (2)

- hugh laury (2)

- ian frazier (2)

- imf (2)

- immelt (2)

- indymac (2)

- iolta (2)

- jamie dimon (2)

- jimmy cayne (2)

- john mack (2)

- kellerman (2)

- lobbying (2)

- loonie (2)

- magnetar (2)

- marcellus shale (2)

- marselus shale (2)

- mcCain (2)

- medicare (2)

- merton.mit (2)

- milton friedman (2)

- neil bortz (2)

- notes from natural gas country (2)

- nuclear power generation (2)

- patrick french (2)

- paumgarten (2)

- pelosi (2)

- peter bernstein (2)

- phil in the mountains of kyushu (2)

- phillip schuck (2)

- philosophy (2)

- pnc (2)

- power grid (2)

- ratigan (2)

- rebecca Worple pictures (2)

- regions financial (2)

- regulation (2)

- rick santelli (2)

- robert shiller (2)

- rolling stone (2)

- schumer (2)

- schwab (2)

- securitization (2)

- seeking alpha (2)

- shadow banking system (2)

- sir allen stanford (2)

- south ossetia (2)

- stanley fish (2)

- stated income loans (2)

- steen (2)

- stress tests (2)

- structured finance (2)

- taleb (2)

- talf (2)

- too big to fail (2)

- treasury (2)

- troubled asset recovery plan (2)

- trusts (2)

- twitter (2)

- veverka (2)

- walter noel (2)

- water (2)

- weatherization (2)

- wells fargo (2)

- whitney tilson (2)

- william cohan (2)

- world affairs (2)

- 1040 (1)

- 12 angry men (1)

- 60 minutes (1)

- Daschle (1)

- December (1)

- Detroit (1)

- Dirty tricks (1)

- Dmitry Orlov (1)

- Econned (1)

- Electricity (1)

- EnCana (1)

- February (1)

- Gold Standard (1)

- Irremedial (1)

- January (1)

- Jr. (1)

- Judith Timson (1)

- Kevin Hassett (1)

- McFadden Act (1)

- National City (1)

- Negrych (1)

- No There There (1)

- November (1)

- Peter Baker (1)

- Rob portman (1)

- September (1)

- Surowiecki (1)

- T. Boone Pickens (1)

- TWITTER DAY capers (1)

- Teddy Roosevelt (1)

- The Flash Guys (1)

- VaR (1)

- WEP (1)

- WPA (1)

- ` (1)

- aa (1)

- aaron pressman (1)

- above the law (1)

- acorn (1)

- adwords (1)

- afghanistan (1)

- africa trip (1)

- aging (1)

- ai (1)

- ajay kapur (1)

- ajit jain (1)

- aligned interest partnerships (1)

- allegheny (1)

- ambient (1)

- american electric power (1)

- anandarko (1)

- andrew j hall (1)

- andrew lo (1)

- andy redleaf (1)

- anne hathaway (1)

- annuities (1)

- apc (1)

- attorney review (1)

- ayp (1)

- ayres (1)

- bachus (1)

- barofsky (1)

- baseball (1)

- basis_of_stocks (1)

- ben stein (1)

- best line of the day (1)

- bill ayres (1)

- bill gates (1)

- bill o'reilly (1)

- bill youngclaus (1)

- blackstone group (1)

- blankfein (1)

- blodget (1)

- blodgett (1)

- bob woodward (1)

- books and entertainment (1)

- brown-kaufman (1)

- bruce harlamert (1)

- bully points (1)

- buy and hold (1)

- california (1)

- canadian banks (1)

- canadian dollar (1)

- carlyle group (1)

- carol loomis (1)

- casa batllo picture (1)

- cds.money market (1)

- charles ortel (1)

- charles taylor (1)

- chesapeake energy (1)

- chicago (1)

- china (1)

- christopher hitchens (1)

- city-data (1)

- cleaving in two (1)

- closing costs (1)

- cloud computing (1)

- cng (1)

- cobra (1)

- colin powell (1)

- collar funds (1)

- colors (1)

- columbia gas (1)

- commercial property (1)

- communitarian (1)

- conan obrien (1)

- concrete (1)

- conocophilips (1)

- consumer financial product agency (1)

- contracts (1)

- cooking (1)

- corporate law (1)

- cottage ownership (1)

- cox (1)

- creditaig.credit default swaps (1)

- daily normals (1)

- dan kucera (1)

- david corn (1)

- david einhorn (1)

- david faber (1)

- david frum (1)

- david gray (1)

- david gu (1)

- david kessler (1)

- dayton daily news (1)

- default option (1)

- deficit (1)

- discount rate mismatch (1)

- divorce (1)

- dmitri young (1)

- douthat (1)

- dov seidman (1)

- due diligence (1)

- dzhugashvili (1)

- earmarks (1)

- earthquake (1)

- edmund andrews (1)

- education (1)

- effrat (1)

- el-erian (1)

- ellen brown (1)

- emma (1)

- equities (1)

- eric holder (1)

- estate planning (1)

- estate taxes (1)

- ethics (1)

- european union (1)

- everything relates to everything (1)

- ewe reinhardt (1)

- exceptionalism (1)

- extend and pretend (1)

- ezra merkin (1)

- f (1)

- facebook fiasco (1)

- fairenergyohio.org (1)

- fault swaps (1)

- feith (1)

- financial engineering (1)

- finland (1)

- first energy (1)

- fitzgerald (1)

- fixed income (1)

- fonts (1)

- food (1)

- foreclosures (1)

- fracking (1)

- fuchs (1)

- futures chain (1)

- game face (1)

- gary kaminski (1)

- gasoline (1)

- gawande (1)

- gazprom (1)

- gerry spence (1)

- glen beck (1)

- good writing; what we learn when special people die (1)

- greek debt (1)

- gregg (1)

- gs; (1)

- gwyn morgan (1)

- hdd (1)

- heroes (1)

- hilda solis (1)

- home buyer tax credit (1)

- homes (1)

- igs (1)

- index funds (1)

- india (1)

- inflation (1)

- infrastructure (1)

- interest rate swaps (1)

- investment neighborhood concept (1)

- iphone+facebook (1)

- ireland (1)

- irs (1)

- james simons (1)

- john burns (1)

- john cassidy (1)

- john_paulson (1)

- jon stewart (1)

- jose manuel tesoro (1)

- julian epstein (1)

- kagan (1)

- karl icahn (1)

- kate middleton (1)

- kate winslet (1)

- ken lewis (1)

- kevin drum (1)

- lafley (1)

- lawyering (1)

- leonie benesch (1)

- liddy (1)

- limiting wall street salaries (1)

- linda greenhouse (1)

- liquidity (1)

- listen up (1)

- lists (1)

- livingwiththeoldies (1)

- lynn a stout (1)

- macArthur (1)

- madmoneyrecap.com (1)

- maira kalman (1)

- malcolm gladwell (1)

- managed futures (1)

- manhattan institute (1)

- mark everson (1)

- mark-to-market rule (1)

- martin act (1)

- mcallen texas (1)

- mcconnell (1)

- meachem (1)

- medicaid (1)

- memory lane (1)

- mergers and acquisitions (1)

- mf global;corzine; Masters of the Universe (1)

- michael jackson (1)

- mike demmer (1)

- mike mayo (1)

- mit (1)

- mit technology review (1)

- mold (1)

- mommy (1)

- money market funds (1)

- moral hazard (1)

- mother jones (1)

- mozilo (1)

- msnbc (1)

- muppets (1)

- mutual funds (1)

- myth of the great war (1)

- nagornay (1)

- naipaul (1)

- nassim taleb (1)

- nationalization (1)

- ncaa (1)

- new construction (1)

- nicholas dawidoff (1)

- nick grealy (1)

- nopec (1)

- not misleading cnbc ads (1)

- not sure (1)

- november 2010 elections (1)

- nymex (1)

- oil sands (1)

- oil spill in gulf (1)

- options (1)

- orange county (1)

- orman (1)

- p&g (1)

- packer (1)

- pakistan (1)

- passive houses (1)

- patrick-taylor plan (1)

- pension funds (1)

- peter weinberg (1)

- phillip blond (1)

- phisosophy (1)

- pico iyer (1)

- pictures (1)

- planes (1)

- plutomomics (1)

- powers of attorney (1)

- prechter (1)

- primal image (1)

- primary care doctors (1)

- procedure (1)

- progress energy (1)

- quants (1)

- queen elizabeth (1)

- quiet zones (1)

- rahm (1)

- randazzo (1)

- random sayings (1)

- randum notes; Hot Air (1)

- ratings (1)

- regulatory capture (1)

- renminbi (1)

- rent scams (1)

- repo 105 (1)

- residential counteroffer (1)

- restoring wireless (1)

- retail (1)

- reunion (1)

- rice v igs (1)

- roger altman (1)

- ron insana (1)

- ross serkin (1)

- roubina (1)

- rtichard posner (1)

- russian winter (1)

- s and p (1)

- sallie mae (1)

- sarah brightman (1)

- saskia de brauw (1)

- saturday night live (1)

- satyajit das (1)

- schadenfreude (1)

- science (1)

- sean miller (1)

- segal (1)

- silver (1)

- single payer system (1)

- singleism (1)

- sistine chapel (1)

- small business (1)

- smart metering (1)

- soros (1)

- speculation (1)

- springfield township (1)

- stalin (1)

- steele (1)

- steidlmayer (1)

- stenfors (1)

- steven g breyer (1)

- steven schwartzman (1)

- stewart (1)

- stiglitz (1)

- strauss-kahn (1)

- strictly local (1)

- susan jacoby (1)

- tabula rasa (1)

- tanenhaus (1)

- tanta (1)

- target date funds (1)

- taxes (1)

- ted forstmann (1)

- ten things (1)

- tett (1)

- thamel (1)

- the haggler (1)

- the reader (1)

- thomas jefferson (1)

- thomas lee (1)

- thomas montague (1)

- thomas ricks (1)

- timeline. laffley (1)

- timothy egan (1)

- tivo (1)

- tod_x;Duke Energy (1)

- todx (1)

- tom archdeacon (1)

- tom daschle (1)

- tom wilson.allstate (1)

- trains and automobiles (1)

- travel insurance (1)

- ultra (1)

- ung (1)

- united states steel (1)

- vanity fair (1)

- vatican (1)

- verizon (1)

- victoria falls (1)

- victorian homes (1)

- w (1)

- wall street (1)

- washinton mutual (1)

- whitebox (1)

- wilpon (1)

- wtrg (1)

- wwII. flash crash (1)

- www.rule26a1.com (1)

- x (1)

- year_end (1)

- zambia (1)

- zardari (1)